In my previous post I noted that Krugman's argument about capital-biased technological change doesn't really warrant his conclusion--that we should tax capital income to finance entitlements. Perhaps a more succinct summary of my point would be that Krugman's argument directly contradicts the best known result from the Ramsey optimal tax literature (named after Frank P. Ramsey, the economist who started the literature in the 1920s), which is that in the long run we should cut capital gains taxes to zero.

The problem with the Ramsey model, however, is that it does not allow for heterogeneity between households, nor does it allow for non-linear tax functions. This is highly problematic since that makes the Ramsey model basically useless both for representing the real world--the tax function in the US is actually highly non-linear--as well as for studying income inequality. There is, however, a completely alternative modeling paradigm for studying optimal tax policy that allows for both non-linearity and heterogeneity, which I will call the Mirrlees literature (after economist James Mirrlees, who started the literature in the 1970s).

I will attempt to summarize the Mirrlees results for capital taxation: interest income and dividends should be taxed at highly progressive rates, but capital gains remains a big question mark. There are some cute things you can do to produce a model in which the optimal capital gains tax is non-zero--usually somewhere in the 2% to 5% range--but they really don't take into account the reality that capital gains income gets super-concentrated in a few number of people. On the other hand, we don't want to significantly distort the accumulation of capital over time.

I have been toying with a policy proposal that aims to rectify the two concerns--the Ramsey concern about arbitrage and accumulation of capital, and Krugman's concern about wealth inequality. My proposal is to institute a moderately high capital gains tax of, say, 35%, but also include a high life-time deductible amount so that households don't pay any capital gains tax on the first, say, $1 million of capital gains income over their lifetimes. Essentially this creates a progressive capital gains tax that differs from typical progressive taxes in the fact that the tax brackets are determined by life-long capital gains, not annual gains. This eliminates the problem that arises with taxing annual capital gains at progressive rates, which results in distorting investment incentives in favor of short-run rather than long-run investments.

Strictly speaking, the Mirrlees literature clearly proves that my policy is sub-optimal: it would result in shifting some of the risk from high to low-income households when the optimal thing to do is just the opposite. However, the policy side-steps some of the more dubious (In my opinion) aspects of the Mirrlees models, and would achieve a reduction in wealth inequality without necessarily penalizing new capital formation. That is, so long as the life-time deductible amount is high enough, we can achieve both a substantial amount of redistribution and the same level of capital formation as in the zero-tax equilibrium (depending somewhat on how risk aversion and income are related in household preferences). Intuitively, my reasoning here is that any profitable investments foregone by the rich due to the high marginal tax can be taken up by the poorer households who have not yet reached the $1 million life-time limit and therefore face a 0% marginal tax rate. This tax policy would distort investments to favor smaller amounts by more households (that is, a more even distribution), but unlike the progressive annual tax is not skewed towards less overall investments, nor to shorter-run investments.

The problem with the Ramsey model, however, is that it does not allow for heterogeneity between households, nor does it allow for non-linear tax functions. This is highly problematic since that makes the Ramsey model basically useless both for representing the real world--the tax function in the US is actually highly non-linear--as well as for studying income inequality. There is, however, a completely alternative modeling paradigm for studying optimal tax policy that allows for both non-linearity and heterogeneity, which I will call the Mirrlees literature (after economist James Mirrlees, who started the literature in the 1970s).

I will attempt to summarize the Mirrlees results for capital taxation: interest income and dividends should be taxed at highly progressive rates, but capital gains remains a big question mark. There are some cute things you can do to produce a model in which the optimal capital gains tax is non-zero--usually somewhere in the 2% to 5% range--but they really don't take into account the reality that capital gains income gets super-concentrated in a few number of people. On the other hand, we don't want to significantly distort the accumulation of capital over time.

I have been toying with a policy proposal that aims to rectify the two concerns--the Ramsey concern about arbitrage and accumulation of capital, and Krugman's concern about wealth inequality. My proposal is to institute a moderately high capital gains tax of, say, 35%, but also include a high life-time deductible amount so that households don't pay any capital gains tax on the first, say, $1 million of capital gains income over their lifetimes. Essentially this creates a progressive capital gains tax that differs from typical progressive taxes in the fact that the tax brackets are determined by life-long capital gains, not annual gains. This eliminates the problem that arises with taxing annual capital gains at progressive rates, which results in distorting investment incentives in favor of short-run rather than long-run investments.

Strictly speaking, the Mirrlees literature clearly proves that my policy is sub-optimal: it would result in shifting some of the risk from high to low-income households when the optimal thing to do is just the opposite. However, the policy side-steps some of the more dubious (In my opinion) aspects of the Mirrlees models, and would achieve a reduction in wealth inequality without necessarily penalizing new capital formation. That is, so long as the life-time deductible amount is high enough, we can achieve both a substantial amount of redistribution and the same level of capital formation as in the zero-tax equilibrium (depending somewhat on how risk aversion and income are related in household preferences). Intuitively, my reasoning here is that any profitable investments foregone by the rich due to the high marginal tax can be taken up by the poorer households who have not yet reached the $1 million life-time limit and therefore face a 0% marginal tax rate. This tax policy would distort investments to favor smaller amounts by more households (that is, a more even distribution), but unlike the progressive annual tax is not skewed towards less overall investments, nor to shorter-run investments.

Krugman has a theory that "capital-biased" technological change is responsible for the fact that in the last few decades an increasing share of aggregate income (GDP) has gone to the owners of capital, instead of workers. That point, by itself, is almost surely true--the trend he references is pretty visible in the data, and it seems to me almost certain that it is the result of changes in production methods that rely more heavily on capital. But then Krugman says this:

Here is the graph Krugman posted:

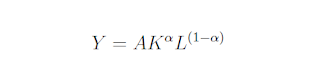

That tells me that he has in mind something similar to the cobb-douglas production function:

where Y is GDP, K is capital, L is labor, and alpha and A are technology parameters. Most economic literature assumes that technological growth comes from increases in A holding alpha constant. This is clearly invalidated by the data, since (as it turns out) alpha is equal to capital's share of aggregate income. So since that share is increasing in the past few decades, alpha must be increasing. Holding capital and labor supply (as well as the parameter A) constant, an increase in alpha would graphically look like a movement from "technology A" to "technology B" in krugman's graph.

where Y is GDP, K is capital, L is labor, and alpha and A are technology parameters. Most economic literature assumes that technological growth comes from increases in A holding alpha constant. This is clearly invalidated by the data, since (as it turns out) alpha is equal to capital's share of aggregate income. So since that share is increasing in the past few decades, alpha must be increasing. Holding capital and labor supply (as well as the parameter A) constant, an increase in alpha would graphically look like a movement from "technology A" to "technology B" in krugman's graph.

BUT! Krugman is wrong in saying that wages fall as a result of an increase in alpha. Yes, he is right that the wage equals the slope of the curve in the graph. But the graph is deceptive--in reality the wage will rise!

I can't believe I'm the first economist to point this out. Fred Mosely and Nick Rowe both weighed in and, in my humble opinion, had nothing useful to say. But no one seems to have pointed out that Krugman's problem is that he is assuming that capital is fixed, when in reality we would expect the steady state equilibrium level of capital to rise in response to an increase in capital's share of income (alpha). Maybe that is what Rowe was hinting at here, though if so he's quite cryptic about it.

I'm relying on a series of well known results in macroeconomics, so for the non-math readers, here is the result: any capital-biased technological change will cause investors to invest in producing more capital, because the return to capital is now much higher than before (intuitively, they are more willing to give up current consumption to invest in capital now). This means that the capital stock rises to a new equilibrium value. Capital and labor are complements in production, so an increase in the capital stock also increases the returns to labor, causing wages to rise. While it is true that total output rises more than wages do, meaning that workers earn a smaller share of GDP, Krugman is absolutely wrong to suggest that workers are worse off than before--in fact, their incomes do rise, possibly quite substantially.

Anyway, here is the math (after the jump):

"if it’s strongly enough capital-biased, they [workers] can actually be made worse off"

which is absolutely, unbelievably wrong.

That tells me that he has in mind something similar to the cobb-douglas production function:

BUT! Krugman is wrong in saying that wages fall as a result of an increase in alpha. Yes, he is right that the wage equals the slope of the curve in the graph. But the graph is deceptive--in reality the wage will rise!

I can't believe I'm the first economist to point this out. Fred Mosely and Nick Rowe both weighed in and, in my humble opinion, had nothing useful to say. But no one seems to have pointed out that Krugman's problem is that he is assuming that capital is fixed, when in reality we would expect the steady state equilibrium level of capital to rise in response to an increase in capital's share of income (alpha). Maybe that is what Rowe was hinting at here, though if so he's quite cryptic about it.

I'm relying on a series of well known results in macroeconomics, so for the non-math readers, here is the result: any capital-biased technological change will cause investors to invest in producing more capital, because the return to capital is now much higher than before (intuitively, they are more willing to give up current consumption to invest in capital now). This means that the capital stock rises to a new equilibrium value. Capital and labor are complements in production, so an increase in the capital stock also increases the returns to labor, causing wages to rise. While it is true that total output rises more than wages do, meaning that workers earn a smaller share of GDP, Krugman is absolutely wrong to suggest that workers are worse off than before--in fact, their incomes do rise, possibly quite substantially.

Anyway, here is the math (after the jump):

I recently realized something about the Affordable Care Act that no one else seems to have noticed: it implicitly expands Medicare coverage for seniors.

To be clear, there is no actual provision increasing the disbursements from the Medicare trust funds. However, the law does implicitly subsidize healthcare for older adults. It does this through a combination of seemingly unrelated provisions. The first is a provision that specifies that insurance premiums for older adults cannot cost more than three times as much as those for younger adults. This means that premiums for old adults would fall, while those for young adults would rise, sometimes substantially. However, the healthcare law also grants subsidies for those making up to 400% of poverty level to purchase health insurance. For reference, 400% of poverty is the median household income, and that group includes a disproportionate share of younger adults because household income rises with age, meaning that in effect, the subsidies will be compensating young adults for having to pay for senior's healthcare through higher premiums. In other words, the law could have achieved essentially the same result by simply offering those older adults in the 60 to 65 year old range with a voucher to apply towards their health insurance.

This brings us back to a common theme in healthcare economics. Namely, that the private sector is pushing the highest riskpools onto the government. I explained here that Ryancare--Rep. Paul Ryan's plan to replace Medicare with an optional voucher system--would cause lower risk individuals to pick private insurance, leaving the government saddled with the expenses of an increasingly costly pool of seniors. We will see this in action with the ACA, though indirectly. Insurance companies will shift the cost of high-risk pools onto those receiving government subsidies, meaning that in effect, the government will absorb the cost of high risk individuals.

To be clear, there is no actual provision increasing the disbursements from the Medicare trust funds. However, the law does implicitly subsidize healthcare for older adults. It does this through a combination of seemingly unrelated provisions. The first is a provision that specifies that insurance premiums for older adults cannot cost more than three times as much as those for younger adults. This means that premiums for old adults would fall, while those for young adults would rise, sometimes substantially. However, the healthcare law also grants subsidies for those making up to 400% of poverty level to purchase health insurance. For reference, 400% of poverty is the median household income, and that group includes a disproportionate share of younger adults because household income rises with age, meaning that in effect, the subsidies will be compensating young adults for having to pay for senior's healthcare through higher premiums. In other words, the law could have achieved essentially the same result by simply offering those older adults in the 60 to 65 year old range with a voucher to apply towards their health insurance.

This brings us back to a common theme in healthcare economics. Namely, that the private sector is pushing the highest riskpools onto the government. I explained here that Ryancare--Rep. Paul Ryan's plan to replace Medicare with an optional voucher system--would cause lower risk individuals to pick private insurance, leaving the government saddled with the expenses of an increasingly costly pool of seniors. We will see this in action with the ACA, though indirectly. Insurance companies will shift the cost of high-risk pools onto those receiving government subsidies, meaning that in effect, the government will absorb the cost of high risk individuals.

John Cochrane makes a good point, though as he often does, not necessarily with the right reasoning. The Eurozone recently reached an agreement that would make the European Central Bank a regulatory authority over banks across the Eurozone to try to prevent systemic risks like those that caused the 2007 recession. According to the Wall Street Journal:

To be honest, this verymuch confuses me. Cochrane seems to feel that regulation is only needed to protect banks from the risk of sovereign debt--shouldn't banks be just as cautious (or reckless) buying government bonds as they are with private assets? At any rate, Cochrane goes on to explain why he thinks it is a bad idea to put the ECB in charge of this:

Moreover, Cochrane's argument is a strawman. He's invented a function he wants the ECB to carry out, and then criticized the results of a regulatory regime that exists only in his mind. In reality, the regime will empower the ECB to regulate capital requirements and nationalize (internationalize?) failing banks. The problem with this, which Cochrane failed to mention, is that central banks rely on cozy relationships with private banks. This is clearest with the Federal Reserve in the US, where much of the policy-making body is actually chosen by the private banks, who appoint the boards of directors of each of the Federal Reserve banks, and indirectly pick their presidents, who sit on the FOMC. The ECB has a similar problem since its governing council consists mostly of the heads of the 17 national banks within the European central bank system. But, in Europe, this problem is muted by the fact that these bank heads are usually (perhaps always?) political appointments rather than chosen by the banking industry itself.

However, even so, the central banks are actively involved in private bank markets, often making loans to banks, buying and selling assets to and from them, and serving as their clearing house. The result, established in much economic research, is that central banks often relax regulations at the request of private banks. The perfect example is the Federal Reserve's steady reduction of reserve requirements, which studies have shown to be a response to pressure by private banks.

For most of what the central bank does, this cozy relationship with private banks is entirely appropriate. The banks want low inflation and low unemployment as much as everyone else. But it means that the central bank is incapable of serving as a bank regulator, which requires enacting regulations that banks don't want to accept. For that purpose you need an outside agency that has no stake in the private banks, and who can take a dispassionate look at their balance sheets.

That conflict of interest is the reason I oppose portions of Frank-Dodd financial reform that expanded the Fed's regulatory role, as well as this new European analogue. I fully expect the ECB to lower, not raise, capital requirements, in response to pressure from banks. I expect them to prop up rather than nationalize failing banks. And the Fed will do the same.

In my view, the regulatory regime should consist of a central bank that uses monetary policy alone--buying assets and serving as lender of last resort--to keep all banks out of bankruptcy, and an independent regulator (like the FDIC) to swoop in and nationalize those that are being kept alive by the central bank's monetary lifesupport.

"...the European Central Bank would start policing the most important and vulnerable banks in the eurozone...the ECB will be able to force banks to raise their capital buffers and even shut down unsafe lenders."Cochrane has some suggestions on the type of regulating they need:

"...it should protect the banking system from sovereign default. It should declare that sovereign debt is risky, require marking it to market, require large capital against it, and it should force banks to reduce sovereign exposure to get rid of this obviously "systemic" "correlated risk" to their balance sheets. (They can just require banks to buy CDS, they don't have to require them to dump bonds on the market. This is just about not wanting to pay insurance premiums.) It should do for the obvious risky elephant in the room exactly what bank regulators failed to do for mortgage backed securities in 2006.

Moreover, it should encourage a truly European market. Greek, Spanish, Italian banks failing is no problem if large international banks can swoop in, pick up the assets, and open the doors the next day. Bankruptcy is recapitalization. Greece needs a national banking system as much as Chicago (same population) does..."

To be honest, this verymuch confuses me. Cochrane seems to feel that regulation is only needed to protect banks from the risk of sovereign debt--shouldn't banks be just as cautious (or reckless) buying government bonds as they are with private assets? At any rate, Cochrane goes on to explain why he thinks it is a bad idea to put the ECB in charge of this:

"The right arm of the ECB should be protecting the banking system in this way. But the left arm of the ECB is using banks as sponges for sovereign debt."That's the crazy part of his argument. For one, the ECB can't force the banks to increase their risk exposure to sovereign debt--it can certainly induce them to buy the bonds by offering guarantees that reduce the risk, but that means they aren't being exposed to that risk. But the bigger point is this: I doubt it matters whether the banks are exposed to the risks directly. The risks from sovereign default are just as harmful if the investors were individuals that own and deposit in the big banks, or if they were the big banks themselves. Or to put this differently, governments are way more systemically more important than any of the banks.

Moreover, Cochrane's argument is a strawman. He's invented a function he wants the ECB to carry out, and then criticized the results of a regulatory regime that exists only in his mind. In reality, the regime will empower the ECB to regulate capital requirements and nationalize (internationalize?) failing banks. The problem with this, which Cochrane failed to mention, is that central banks rely on cozy relationships with private banks. This is clearest with the Federal Reserve in the US, where much of the policy-making body is actually chosen by the private banks, who appoint the boards of directors of each of the Federal Reserve banks, and indirectly pick their presidents, who sit on the FOMC. The ECB has a similar problem since its governing council consists mostly of the heads of the 17 national banks within the European central bank system. But, in Europe, this problem is muted by the fact that these bank heads are usually (perhaps always?) political appointments rather than chosen by the banking industry itself.

However, even so, the central banks are actively involved in private bank markets, often making loans to banks, buying and selling assets to and from them, and serving as their clearing house. The result, established in much economic research, is that central banks often relax regulations at the request of private banks. The perfect example is the Federal Reserve's steady reduction of reserve requirements, which studies have shown to be a response to pressure by private banks.

For most of what the central bank does, this cozy relationship with private banks is entirely appropriate. The banks want low inflation and low unemployment as much as everyone else. But it means that the central bank is incapable of serving as a bank regulator, which requires enacting regulations that banks don't want to accept. For that purpose you need an outside agency that has no stake in the private banks, and who can take a dispassionate look at their balance sheets.

That conflict of interest is the reason I oppose portions of Frank-Dodd financial reform that expanded the Fed's regulatory role, as well as this new European analogue. I fully expect the ECB to lower, not raise, capital requirements, in response to pressure from banks. I expect them to prop up rather than nationalize failing banks. And the Fed will do the same.

In my view, the regulatory regime should consist of a central bank that uses monetary policy alone--buying assets and serving as lender of last resort--to keep all banks out of bankruptcy, and an independent regulator (like the FDIC) to swoop in and nationalize those that are being kept alive by the central bank's monetary lifesupport.