Some confusion about multiple equilibria

One of the best kept secrets in economics is that almost any result can actually be intuited by thinking in terms of one or more Edgeworth Boxes. Indeed, almost all the mistakes economists make could be caught if only they had sketched out an Edgeworth Box or two. So here's the Edgeworth box:

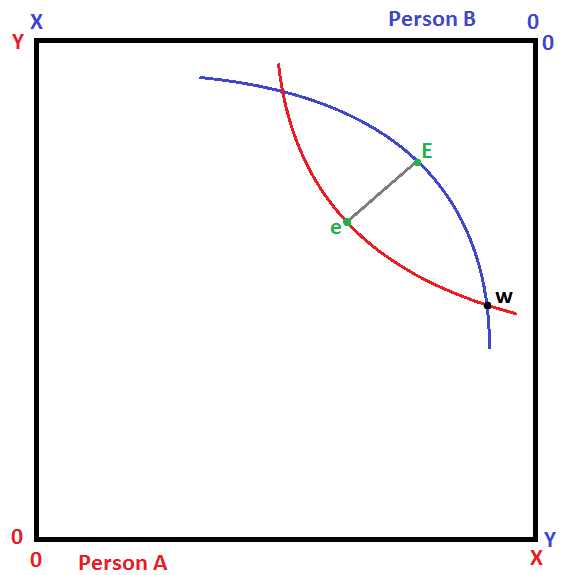

In the edgeworth box above, I've endowed this economy with an initial distribution w that is highly unequal, where Person A has more of y and way more of x than person B. But this is an exchange economy, so they will not stay there. Both A and B want to move to preferred indifference curve, and the lense-shaped region between the two indifference curve represents all the different points where both A and B would be better off than if they stayed at w. The "contract curve" shown in grey, (the line segment eE) represents the set of points where we've exhausted any potential for further gains from trade. The indifference curves at any of those points would be exactly tangential to eachother, so that there is no interior lense-shaped space where both individuals can be better off. Hence, each point on the contract curve represents an equilibrium in this model.

It turns out that multiple equilibria are excruciatingly common in economics. Even in this, the most basic possible model with well-defined preferences, only two agents and two goods, no production, there are infinitely many equilibria. And they cover a pretty large range, from an almost egalitarian equilibrium at e to extreme inequality at E. I've encountered some economists who have argued that the existence of multiple equilibria is a cause of economic inefficiency, or a reason to believe that government intervention would be exceptionally effective. Both claims are totally, inexcusably false. Any point along the contract curve is Pareto Efficient. Moreover, there is no theoretical reason in this model to suppose that any kind of government policy would have any effect whatsoever over which equilibrium Person A and Person B trade to. This model predicts that they will trade to one of the points on the contract curve, but gives absolutely no prediction of any kind as to which of those points.

This gets at the crucial point about multiple equilibria in general: the are a huge problem for economists, but not in general a problem for economies. Multiple equilibria thwart economists efforts at prediction, but they do not imply that the economy is prone to inefficiency, or that government intervention is required--quite the opposite, those kinds of claims would require that the model produce a single unique equilibrium prediction.

On the other hand, none of this is to say that the existence of multiple equilibria inhibit the effectiveness of government intervention. Let's consider a very simple redistribution policy: at initial endowment w, Person A has way more of x than Person B, so let's redistribtue some of that x away from Person A to Person B by way of lump-sum taxation and transfers. Here's that in an edgeworth box:

The lesson here is this: multiple equilibria inhibit the ability of economists to produce precise predictions. They have nothing whatsoever to do with the effectiveness or ineffectiveness of government interventions, and there is absolutely no basis for claiming that policy can influence which of many equilibria will be realized in the economy.

-http://iriewealthonearth.weebly.com